Economic development in India has

stimulated the demand for Electricity and the

total consumption is expected to reach 15,280

TWh in 2040, from 4,926 TWh in 2012, as per

India Brand Equity Foundation (IBEF). The

demand is expected to be met from all energy

sources like Coal, Oil, Natural Gas, Solar,

Wind, etc. It becomes necessary to increase

the share of renewable energy mix, thereby

establishing more stable and secure critical

infrastructure to facilitate economic growth.

Further, to limit the rise in temperature to

2°C above pre-industrial levels, it becomes

vital to reduce the emissions from Electricity

generation from Conventional Energy

sources. India has set an ambitious target

to set up 227 GW renewable energy sources

by 2022. According to the Renewable Energy

Country Attractiveness index 2018 by EY, the

Indian renewable energy sector is the third

most attractive renewable energy market in

the world. India Energy Outlook 2021 by IEA

has predicted that the Covid-19 pandemic

will drive down the coal and oil demand and

increase renewable energy generation from

Wind and Solar by 15%.

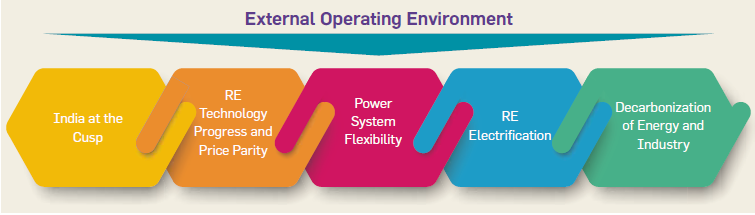

India at the Cusp

India is the third-largest producer and

second-largest consumer of electricity in the

world and has an installed power capacity of

379.13 GW as of February 2021. For 2020-

21, the electricity generation target from

conventional sources was fixed at 1,330 BU,

comprising 1138.533 BU of thermal energy;

hydro energy (140.357 BU) and nuclear

(43.880 BU); and 7.230 BU was imported

from Bhutan. Further, the electrification of

the country will promote the socio-economic

well-being of the people, and the Government

of India is making efforts to electrify every

nook of the country.

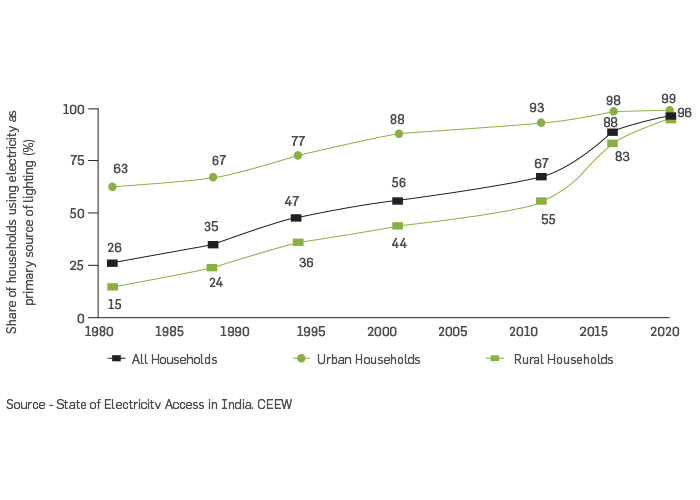

Domestic energy demand is expected to grow

due to increasing industrial growth, nuclear

families, shrinking household sizes, and

urbanization. Policies in India, over the last

decade, have proved effective and accordingly,

96.7 percent of Indian households are now

connected to the grid, with another 0.33

percent relying on off-grid electricity sources.

2.4 percent of Indian households remain

unelectrified (State of Electricity Access in

India, CEEW).

India’s progress on household electricity access (1980-2020)

India will be one of the epicenters of Industrial development in near future.

Further, the growth in commercial space will inflate the electricity demand for

indoor environmental requirements like air conditioning and lighting. Transition

to electrified mobility and industrial applications will also add to the increasing

demand. Government plans to electrify rail routes will add to the demand.

Expected increase in electricity demand in India in the coming years provides

enormous opportunities for Greenko to harness renewable energy.

RE Technology Progress

and Price Parity

The ongoing Climate change is inducing entities to undergo an obligatory

transition from fossil fuels to Renewable energy sources like Solar, Wind, etc.

to limit GHG emissions, increasing sea levels, melting glaciers, and increasing

temperature. Further to ensure energy security, it becomes necessary to

diversify energy sources to reduce the reliance on fossil fuels.

Source- Global energy transformation: A roadmap to 2050, IRENA

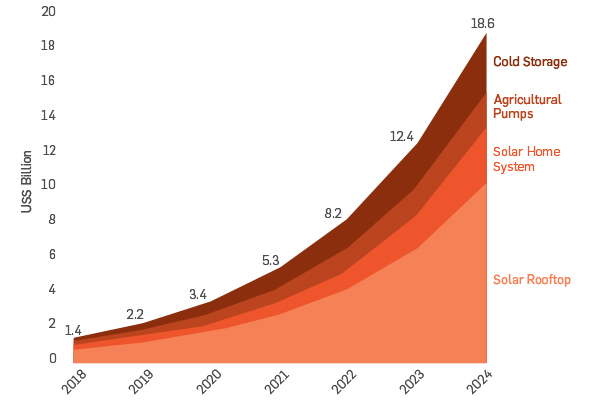

The solar power sector in India is expected to undergo explosive growth in

the upcoming years and IEA states that solar will match coal’s share in the

Indian power sector in two decades. Presently, Solar accounts for less than

4% of India’s electricity generation, and coal is close to 70%. By 2040, they

converge in the low 30%, and this electrifying turnover is attributed to policy

initiatives and targets set by the Government. The Indian Electricity sector is

at the cusp of a Solar Revolution and there is huge potential not only for large

PV plants but, also for small distributed renewable energy sources like solar

Source - The Future of Distributed Renewable Energy in India, Climate Policy Initiative

rooftops, solar pumps, cold storages etc. Solar energy is now the lowest-cost

source of new energy in India. Spain, India, and the Middle East will continue

to be the markets with the lowest solar Levelized cost of electricity (LCOE).

The photovoltaic (PV) systems CAPEX will continue to decline in 2021 by

5% year on year, largely driven by decreasing component prices. Meanwhile,

average module efficiency records continue to increase, surpassing 22.5%

in PERC monocrystalline cell commercial production, and are forecasted to

reach 24% by 2022. Solar energy has the potential to meet the energy needs of

low incomed residential groups and thereby, can also help in achieving 100%

electrification of households. Further, there are various initiatives taken by

stakeholders to trigger the domestic manufacturing of solar panels and this

could even lead to further lowering of price.

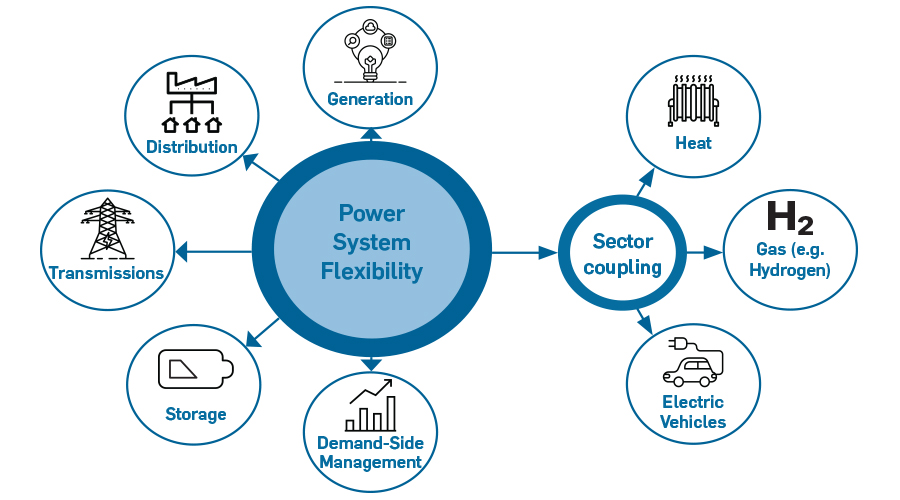

Power System Flexibility –

Need of the Hour

Power system flexibility is defined as the ability of a power system to reliably

and cost-effectively manage the variability and uncertainty of demand and

supply across all relevant timescales. The deployment of variable renewable

energy sources is accompanied by challenges such as increase in system

requirements for balancing supply and demand. To effectively aid the transition

from fossil fuels and ultimately to Net Zero levels, it becomes necessary to

identify and exploit various flexible system integration sources in all stages viz.,

Generation, Distribution, Storage.

Source - IRENA

International experience suggests that a

diverse mix of flexibility investments is needed

for the successful system integration of wind

and solar PV. Operational Complexity rises as

the share of variable renewables rises. Hydro

Power and Pumped Storage systems are

flexible renewable energy sources in India

for a long period. The need for flexible energy

system was realized during the pandemic

and hence, Central Electricity Regulatory

Commission has come up with the regulation

to operate coal-fired power plants with

minimum generation levels at 55%. This has

proved effective in increasing the capability

of coal-fired plants to accommodate VRE.

Supply-side Flexibility system integration

further includes Grid reinforcement and

planning to effectively accommodate VRE

energy generation and several small-scale

initiatives like rooftop net metering, which

has been effective for households. Network

developmental innovations, technology

up-gradation, Research on Modelling and

Optimization, Grid Digitization are further

required to develop resilient, reliable, and

transparent systems.

Energy Storage Systems will play a crucial

role in increasing the system flexibility to

accommodate the demand requirements. The

energy storage market in India witnessed

a demand of 23 GWh in 2018 with 56%

of the battery demand coming from the

power backup inverter segment. The raw

materials for localized battery manufacturing

are limited and this serves as a setback

in integrating flexible storage systems.

Recycling of batteries and others should be

encouraged to drive domestic manufacturing.

Pumped Hydro Energy Storage has been the

most effective energy storage system over

the years and it has now become necessary

to develop small-scale storage devices with

increased efficiency and decreased cost to

aid the smooth transition. This development

would ultimately lead to the large-scale

adoption of Green Energy technologies at all

levels.

RE Electrification

The race to Net Zero 2050 requires the deployment of various renewable

energy technologies and other BoS systems on a massive scale. The changing

scenarios like the decreased cost of RE systems, the flexibility of energy

systems, policy initiatives, and global pressure will lead to a historic shift. The

research to diversify the energy sources will prove effective in exploring new

feasible technologies. The augmentation of flexible systems like making the

Grid systems smarter and resilient from threats will aid in the Re-Electrification

pathways by increasing the share of renewable channels.

Decarbonization of Energy and Industry

Climate change mitigation is one of the key areas for the countries to contribute

to promote sustainable development and ensure the socio-economic well-being

of the general population. GHG emissions are major drivers of global warming

leading to various human ecological consequences. India is one of the largest

energy producers and consumers in the world. Energy Sector accounts for 73%

of GHG emissions which is the result of cumulative energy usage in Iron and

Steel Industries, Petro Chemical Industries, Transport sectors, Residential

and Commercial buildings. This gives rise to the need to shift to low carbon

energy technologies and energy-efficient techniques. Further, the deployment

of renewable energy and subsequent decrease in usage of conventional energy

sources like Coal, Oil, etc will also help in reducing the catastrophic events.

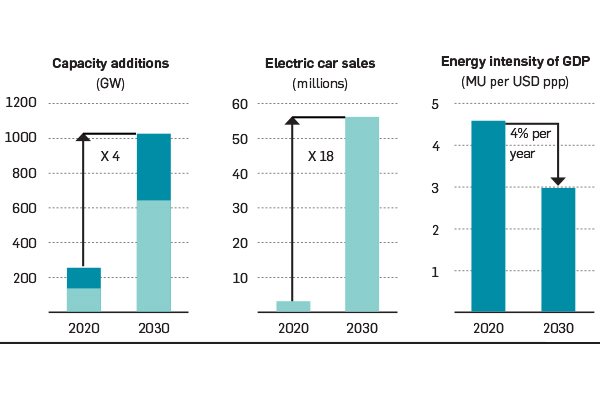

Key clean technologies ramp up by 2030 in the net zero pathway

Note: MU = megajoules; GDP = gross domestic Product in purchasing Power parity

Further to Decarbonizing the electricity

systems, innovations in storage technologies,

electrolyzers, carbon capture systems can aid

the transformative journey. Green Hydrogen

and Molecules are expected to evolve as an

alternative fuel replacing fossils, especially

in energy-intensive industrial sectors. The

exponential growth in the electrolysis project

pipeline in 2020 and the unprecedented

interest around hydrogen as a decarbonization

tool have been driven by a combination of

falling costs and policy support. The declining

cost of low-carbon hydrogen is anticipated

to continue to fall by a further 40% through

2025 due to the falling cost of renewable

electricity. But, the obstacles for tapping this

fuel like electrolysers, transportation of green

hydrogen, and the requirement of renewable

energy for providing the power source are to

be subjugated. Carbon capture, utilisation, and

storage systems are important technological

systems to mitigate global warming by

capturing and storing the emission. Cost

of the technology is a major bottleneck for

effectively utilizing, innovating and providing

policy assistance to speed up the adoption.

Circular Economy practices can also augment

climate change mitigation by increasing

the life cycle of materials and also thereby

reducing the corresponding GHG emissions

associated with the manufacturing process,

transportation of raw materials. Material

Efficiency plays a significant role in promoting

circular economic business models. Take-Make-Waste linear models when replaced

with circular models can have impactful

results in decarbonizing the systems. Life

cycle emissions of solar and wind systems

will also be drastically reduced since a major

portion of emissions is from the Fabrication

of systems. The barriers like Government

regulations, Technological feasibility,

Consumer behaviour, and expectations

should be handled efficaciously to establish

synergies between decarbonization and

circular business models.

Greenko is poised to become a global energy solutions provider with our customer centric and technology-based solution approach. In today’s dynamic world, where major economies and businesses are increasingly focused towards net zero goals, we are well-positioned to deliver a multitude of competitive green energy products including electricity, industrial feedstock and other new-age energy molecules.

Greenko is poised to become a global energy solutions provider with our customer centric and technology-based solution approach. In today’s dynamic world, where major economies and businesses are increasingly focused towards net zero goals, we are well-positioned to deliver a multitude of competitive green energy products including electricity, industrial feedstock and other new-age energy molecules.